Observations: What Nigeria’s riots can tell us about US inflation

Outtake from "Observations: Götterdämmerung"

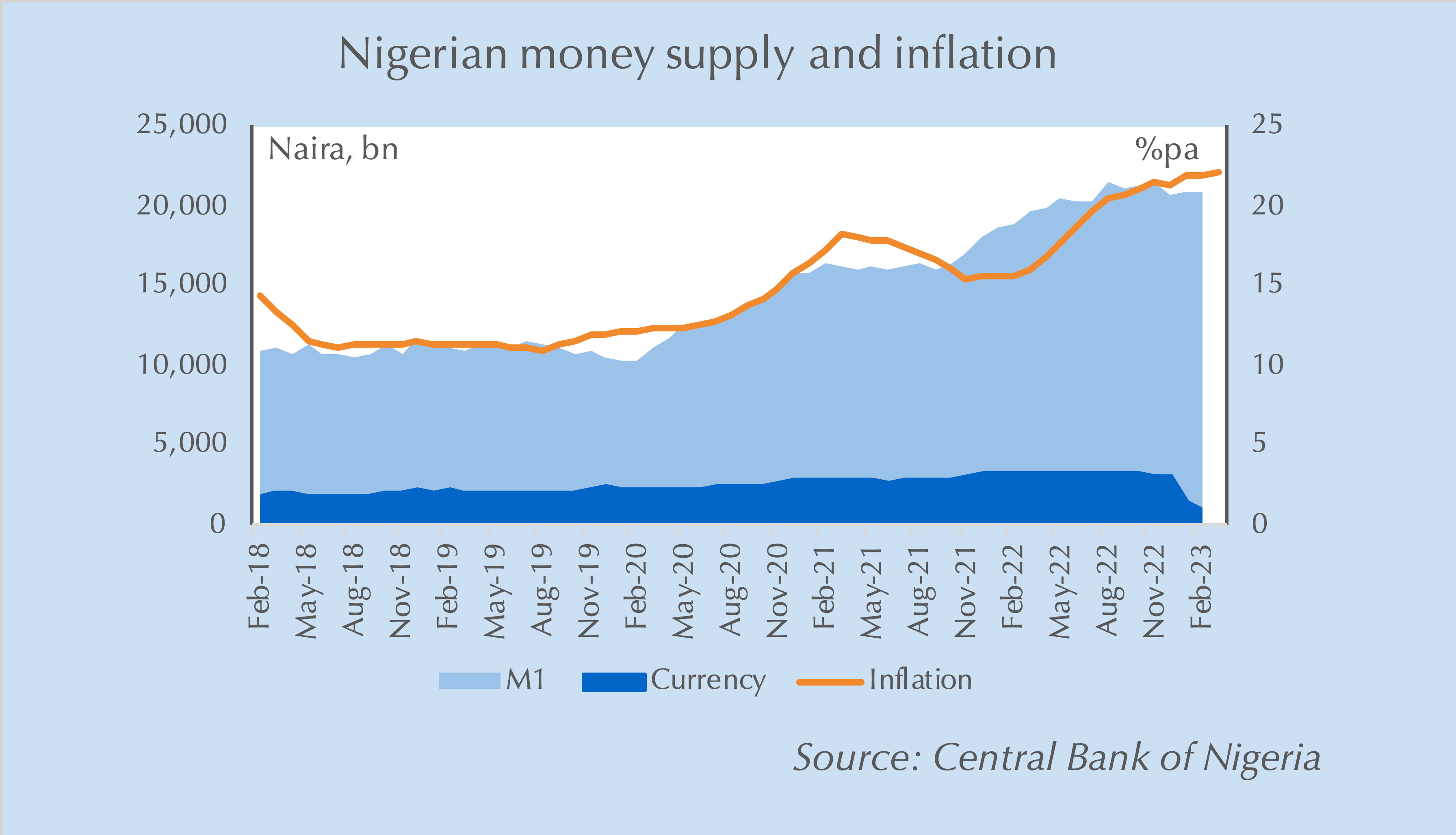

A remarkable natural experiment is taking place in Nigeria that illustrates the extraordinary power of Being is believing effects with useful lessons for inflation in other economies. To curtail counterfeiting, in December, the Central Bank of Nigeria began exchanging existing 200, 500 and 1,000 naira notes for newly designed ones and announced that the older notes would be demonetized at the end of January. However, it failed to print sufficient new notes for the transition and currency in circulation plunged by 69% from November to February (see first chart). While the effect on the total money supply was a smaller 2.3% drop, an estimated 70% of retail trade in Nigeria is conducted in cash transactions,1 and the contraction in currency in circulation provoked rioting across Nigerian cities.

The tragic effects on ordinary Nigerians derive from the potentially counter-intuitive mechanics of Monetary Economics that have important implications for the path of inflation in other countries like the United States. Inflation is determined by the complex interaction of aggregate supply, aggregate demand and, crucially, beliefs. The last one, which I refer to generally as “Being is believing” effects but in this case refers specifically to inflation expectations, is too often neglected. But as the recent experience in illustrates its power. While aggregate supply and demand can “push” or “pull” inflation, beliefs can create it autonomously, often much more powerfully than “real” economic variables. If everyone believes inflation will be higher, producers are much more likely to raise prices and consumers more willing to accept them (without switching brands), regardless of other things going on in the economy.

In Nigeria, this effect was so powerful that the collapse in currency crimped economic activity rather than curtail inflation. As shown in the chart below, inflation has continued to accelerate in Nigeria – to a multi-decade high of 22% in March – even as currency in circulation collapsed. Instead, it appears that retail trade has fallen by an estimated 3%,2 reflecting the “quantity theory of money” that for a given fall in the money supply either inflation or output must fall, or the turnover (velocity) of money must rise. In Nigeria’s case, inflation expectations would not allow inflation to fall, so output and velocity had to adjust instead.

What does this have to do with inflation in the US, UK, and other economies experiencing higher than usual inflation? Readers of Thematic Markets will know the critical role that inflation expectations – Being is believing effects – have played in the shift higher in advanced economy inflation since 2021. Yet, despite consistent evidence from the University of Michigan and New York Fed surveys of consumers that inflation expectations (second chart) are not falling – particularly among the lower-education consumer that led its rise in late 2020 – markets (wrongly in my view) price a rapid return to 2% inflation in the US by next year. Nigeria is not an advanced economy, but human nature and the power of believes is quite constant across societies; economic analysts and markets might do well to heed the lessons Nigeria is illustrating.

This free article is an outtake from Observations: Götterdämmerung, an article for paid subscribers. Thematic Markets research provides differentiated strategic insights into the global political economy and markets based on rigorous fundamental research. If you enjoyed this article and found it thought provoking, please consider subscribing.

“Rewane: Naira Crunch May Cause $18m GDP Loss Per Month,” Dike Onwuamaeze, This Day, 14 February 2023.

Ibid.